Interest Rates and the Lending Market for Commercial Real Estate

Anchor Viewpoints: Q4, 2024

By Steen Watson, President, Anchor Health Capital

Anchor Health Capital (formerly known as Chestnut Funds) manages real estate investment funds that invest in distinct strategies but with a common denominator of investing in middle market real estate alongside operating partners. Chestnut Funds was founded in 2012 after the partners’ collective experience revealed market inefficiencies, that if addressed, could provide meaningful investment opportunities for investors. Now, with five multi-asset funds under management and fundraising for our third medical outpatient building (MOB) fund underway, we remain true to our founding investment thesis.

Challenges within the U.S. commercial real estate market have frequently been linked to issues in the financing markets. For example, during the Great Financial Crisis, difficulties in residential subprime lending extended into the commercial real estate lending market, which was similarly characterized by relaxed lending standards. More recently, the U.S. commercial real estate sector has encountered obstacles due to elevated interest rates stemming from the Federal Reserve's initiatives to curb inflation. These increased interest rates, along with stricter lending standards, have adversely affected commercial real estate values although property operating performance across many sectors remains strong. In this edition of Viewpoints, we examine the effects of recent changes in the financing market and challenges faced by borrowers and lenders because of value declines and higher rates.

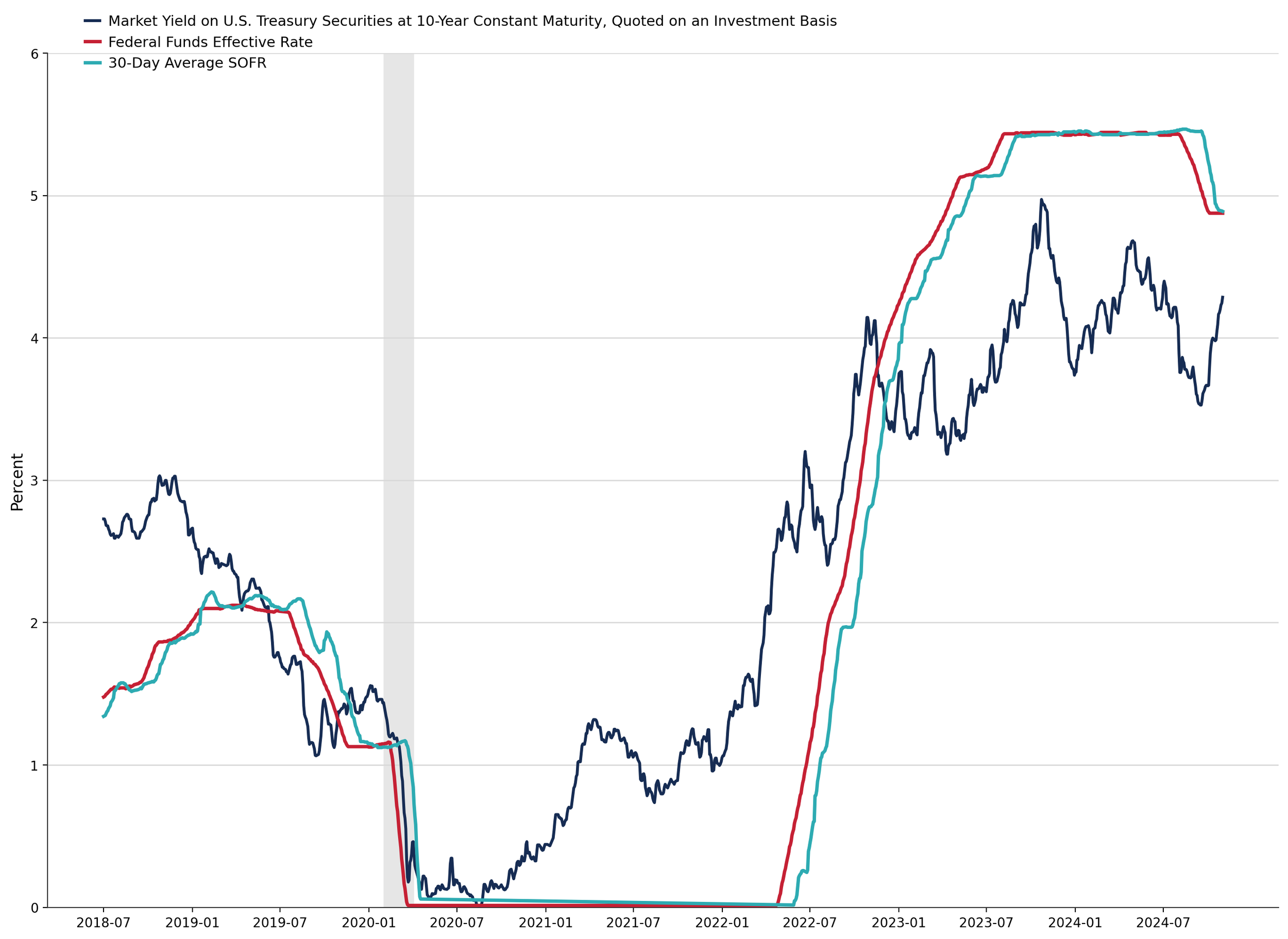

The Interest Rate Picture

The sharp rise in interest rates between 2020 and 2022 resulted primarily from the Federal Reserve’s efforts to fight inflation. At the beginning of and during the COVID pandemic, monetary policy was very accommodative to support the economy. Economic stimulus was also provided through fiscal policy. The combination of this stimulus and supply chain disruptions tied to the pandemic resulted in significant inflation that spurred the Federal Reserve to increase the Federal Funds Rate from almost 0% to 5.33%.

At the same time, the 10-year Treasury rate increased though not to the same extent as the Fed Funds Rate as long term borrowing rates are influenced by many factors tied to future expectations. The sharp rise in interest rates resulting in increased borrowing costs has caused a drop in commercial real estate values. Commercial property prices have fallen by 21% from their mid-2022 peak, according to Green Street.

Sources: Board of Governors of the Federal Reserve System (US); Federal Reserve Bank of New York.

For illustrative purposes only. Data has been approximated and may not reflect exact historical values.

Short-term variable borrowing rates are often tied to the Secured Overnight Financing Rate (SOFR). This index replaced LIBOR and is the index that is primarily used by commercial real estate lenders. Interest rates on variable rate loans are priced as a spread over SOFR. Interest rates may be fixed on long term loans and those rates typically are more closely tied to longer term Treasury yields, plus a spread. As the Federal Reserve has begun to reduce the Fed Funds Rate, long-term rates also declined. Notably and recently, Treasury yields have increased even as short-term rates have declined, primarily, it seems, due to expectations regarding economic growth and inflationary policies that may be pursued by the incoming presidential administration.

Challenges for the Lenders and Borrowers

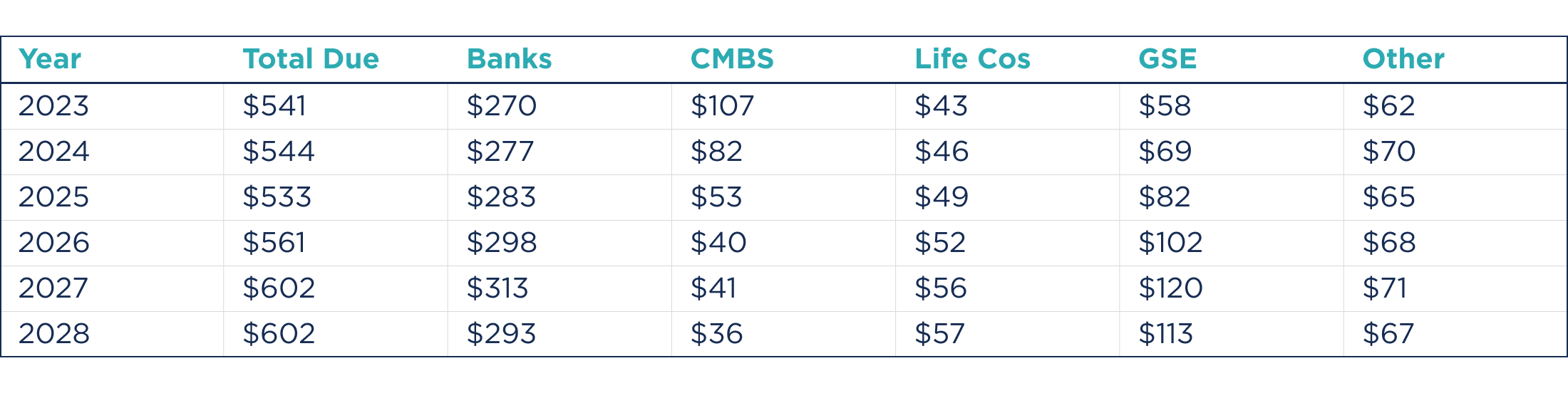

Commercial real estate value declines create challenges for borrowers and lenders when loans mature. Combined with higher interest rates, borrowers may not be able to secure financing in an amount equal to their current loan balance, and if they do, then the interest payments are likely to be significantly higher. In 2023, $541 billion of commercial loans matured. This is the highest amount ever recorded, and the next several years are estimated to have even higher levels of loans maturing. For context, as of Q4 2023 an estimated $4.69 trillion of commercial mortgages are outstanding.

Commercial Mortgage Maturities by Lender Type ($ Billion)

Source: Trepp, Inc., based on Federal Reserve Flow of Funds data

One of the lessons that many lenders appear to have learned from the Great Financial Crisis is that patience pays. This is sometimes referred to pejoratively as “pretend and extend”. But working with borrowers who face challenges refinancing at maturity is rational particularly when property performance remains strong. There is some evidence that this approach is being pursued by many lenders, a hopeful sign for the market.

On the flip side, there’s legitimate concern that some lenders, and particularly small and midsize banks, hold commercial real estate loans on their books that exceed their risk-based capital requirements. Large banks hold relatively lower amounts of commercial real estate loans, in some part because regulatory scrutiny on these lenders is higher and has led them to recognize loan losses. Small and midsize banks have realized almost no losses, suggesting that they are managing challenged loans through extending loans and working with borrowers.

The Outlook

The commercial real estate lending market is affected by numerous factors. Besides the significant number of loan maturities anticipated in the upcoming years, other potential risks are present. These include a potential U.S. recession, prolonged elevated interest rates, and fiscal crises such as expanding deficits or stalled debt ceiling negotiations which may lead to higher Treasury yields. Although value declines have been challenging for commercial real estate owners and investors, property performance has remained robust, resulting in relatively low levels of distressed loans and foreclosures. Given the impending loan maturities and uncertain interest rate climate, sustained strong operating performance driven by continued economic growth is likely key to avoiding further challenges.

Sources

Harvard Business Review. Commercial Real Estate is Headed Toward a Crisis. (July 2024)

Trepp. CRE Mortgage Maturities & Debt Outstanding: $2.81 Trillion Coming Due by 2028. (December 2023) Viewpoints Q4, 2024

Mortgage Bankers Association. Commercial and Multifamily Mortgage Debt Outstanding Increased in Fourth-Quarter 2023. (March 2024)

Green Street. Commercial Property Price Index. (March 6, 2024)

Board of Governors of the Federal Reserve System. Federal Funds Effective Rate. (November 19, 2024)

Board of Governors of the Federal Reserve System. 10 Year Treasury Rate. (November 19, 2024)

Disclaimer

The information contained in this document is intended for informational purposes only and is not intended to provide personalized investment advice or to constitute an offer or solicitation to buy or sell securities or interests in any investment. The charts, graphs, and other information contained herein should not serve as the sole determining factor for making investment decisions.

This document cannot be reproduced, shared, or published in any manner without the prior written consent of Anchor Health Capital (“Anchor”). Unless otherwise indicated, all statements and expressions in this paper are the sole opinion of Anchor and are subject to change without notice. Predictions, forecasts, or outlooks described or implied are forward-looking statements based on certain assumptions, which may prove to be wrong, and/or other events, which were not taken into account, may occur. Any predictions, forecasts, outlooks, opinions, or assumptions should not be construed to be indicative of actual events, which will occur. The opinions and data in this newsletter have been obtained from sources believed to be reliable. Anchor does not warrant the accuracy or completeness of such and accepts no liability for any direct or consequential losses arising from its use.

Investing in securities involves risk of loss and should not be based solely on marketing materials including the information provided herein. Further, depending on the different types of investments there are varying degrees of risk. Private Funds managed by Anchor and their investors should be prepared to bear investment loss, including loss of original investment. There is no assurance that any specific investment or investment strategy utilized by Anchor will be either suitable or profitable for your portfolio. Anchor does not provide personalized or customized investment advice, therefore you are urged to discuss your personal investment situation with the financial professional of your choice before making or changing an investment in a Anchor offering.

Because of the inherent risk of loss associated with investing in any type of securities, Anchor is unable to represent, guarantee, or even imply that its services and methods of analysis can or will predict future results, successfully identify market tops or bottoms, or insulate you from losses due to market corrections or declines.